FX Monthly Outlook – August 2019

Economic Outlook and Summary

The U.S Federal Reserve has recently signaled towards tightening monetary policy, after it cut interest rates for the first time since 2008—by 0.25 percentage points. Although the USD saw a brief decline, the Feds hawkish turn has resulted a rally of up to 1.25 percentage points, since the announcement. Further trade tensions have weighed on the US dollar, as China devalued the Yuan in response to the Trump administration’s tariffs. With the recent escalation in the trade tensions, the U.S Federal Reserve may be required to take a more dovish stance.

The Canadian dollar has seen a sharp decline since it’s July high; however, the Bank of Canada’s decision to hold interest rates should favour the appreciation of the CAD. Although Canada posted a loss of 24,200 jobs for July, a 4.5% wage growth offset the increase in unemployment. Hence, the CAD remains between two opposing environments; whereby healthy domestic conditions demonstrate economic strength, juxtaposed to the external economic downturn. Analysts expect the CAD to appreciate in the near-term, as Bank of Canada proceeds cautiously amid external economic uncertainty.

The US Dollar and the Federal Reserve

Events in July caused a lot more turmoil than usual for financial markets in mid-summer. Global financial markets reacted quickly and negatively to mixed messaging by Federal Reserve Chair Jerome Powell. Financial markets wanted more clarity on the Fed’s commitment to further rate cuts and many were puzzled as to why rates were cut at all given the solid performance of the U.S. economy. Analysts believe the 25 basis-point cut in July should help to offset the impact of a slowing global economy on domestic growth, but it’s likely not enough to insure against the fallout from past tariff actions. A follow-up rate cut in September may be necessary.

After talks broke down during a brief meeting between trade representatives from the U.S. and China, U.S. President Trump called for a 10 % tariff on the remaining $300bn in untariffed Chinese imported goods beginning September 1st. Placing tariffs on the remaining Chinese imported products is likely to negatively impact economic activity and China is likely to retaliate by taking further actions to impede U.S. business activity in the country. China already let their Yuan’s exchange rate depreciate beyond US $7, an important psychological threshold that could send tremors through global financial markets. With no end in sight for trade tensions, any unexpected negative impact on U.S economic performance would likely call for even lower interest rates to help support U.S. economic growth.

The Canadian Dollar and Bank of Canada

Despite falling from it’s July highs, the CAD remains strong as it posts a year-to-date appreciation of 3.2%–down from July’s high of 4.5%. Expectations of further OPEC cuts have developed amid low European inventories, and worsening US-China trade tensions. These developments resulted in a rally of more than 50 basis points from the recent decline. The CAD was also supported by a reported year-over-year wage growth of 4.5 percent—the indicators highest report since January 2009. This increase was enough to offset the loss of 24,200 jobs across Canada in July. Further positivity was demonstrated by the housing market as July demonstrated higher residential investment, supported by lower interest rates. Stable inflation has also supported the Bank of Canada, as they remain relatively neutral in their economic growth estimates of 1.3% for 2019. Overall, the Canadian economy continues to grow at a steady rate, within the control range of 1-3%, despite global slowdowns. The recent momentum suggests the potential for upward movement in the CAD—throughout the second half of 2019. The consensus on the year-end target for USD/CAD remains unchanged at 1.30.

Oil Prices

Oil last month capped its smallest monthly move since 1991 as it was caught between concerns of slowing global demand and fears crude flows from the Middle East may be disrupted. Oil had suffered its steepest one-day drop in more than four years as President Donald Trump abruptly escalated the trade war with China. Concerns over slowing growth has already been reflected in prices, and it remains to be seen whether oil will fall further from here as we have geopolitical risks still lingering in the Middle East. Trump later said America’s new import taxes, will apply to almost all trade with Beijing and tariffs could go well beyond 25%, however Trump left the door open to further talks. If it all goes downhill from here, attention will shift back on OPEC+ to see if the producers will act to deepen their cuts before the current deal expires. OPEC’s output slid in July and is currently at their lowest production level in five years.

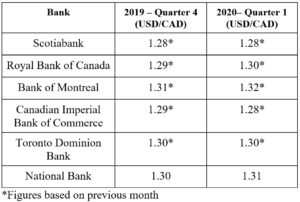

FX Forecast Table – August 2019