FX Monthly Outlook – December 2019

Economic Outlook and Summary

The Federal Reserve proceeded with a neutral stance in their December rate announcement, with the prospect of undertaking additional open market operations—in the form of short-term coupon-bearing securities. Progress in the trade war prompted positive sentiments in the markets as phase one of the agreement will require China to purchase approximately $200 billion in US goods, in exchange for a 7.5% tariff reduction on imported Chinese goods—from 15%. Despite the progress in the trade war, the 16-year high in the US dollar may negatively affect US exports. Therefore, investors will look towards the first half of 2020 to determine the effect of an inflated US dollar.

The Canadian dollar has demonstrated strong gains in early December as it hovers around its highest point in the last month. The Bank of Canada reiterated its neutral stance towards interest rates, acting as one of few countries, globally, to maintain interest rates throughout 2019. With inflation on target at 2%, signing of CUSMA, progress in the trade war, and successful OPEC cuts, investors can expect increased stability from key CAD determinants. However, with the majority of Canada’s financing being derived from currency and deposits, this may indicate a risk-off setting. Going forward, investors should look towards the financing of external deficits as an indicator of investor sentiments in the Canadian economy. Currently, the USDCAD is expected to remain within the 1.32 range towards the end of 1Q20.

The US Dollar and Federal Reserve

The Federal Reserve took a neutral stance in their most recent announcement, as interest rates were maintained at the 1.5-1.75% level. Powell indicated that the neutral stance will likely persist throughout the course of 2020—assuming economic conditions remain broadly consistent. This neutral stance will be in place alongside moderate quantitative easing, with the possibility of purchasing short-term coupon-bearing securities—effectively easing liquidity strains in money-markets. The NMI registered growth at 53.9%, which constitutes a 0.8% reduction from the previous month, indicating a slowdown in growth that was not reflected by recent labour statistics. The unemployment rate marginally decreased to 3.5%, as nonfarm payroll increased by 266,000 in November—beating estimates of 185,000.

Earlier this month, the US and China reached a partial trade deal in phase one of their negotiations. The US agreed to reduce tariffs from 15% to 7.5% on $120 billion of Chinese imports, in addition to cancelling any further tariffs that were planned for December 15th. China, in return, agreed to increase its purchasing of US goods by approximately $200 billion over the next two years—with agricultural spending nearly doubling year-over-year during this period. Despite positivity in the trade war, US exports may be harmed by the resulting strength of their dollar, which is hovering at a 16-year high. Furthermore, the implementation of steel tariffs on Brazil and Argentina may exacerbate this trend, while igniting further trade tensions. Therefore, the increases in the USDCAD may come at the expense of US exports.

The Canadian Dollar and Bank of Canada

The USDCAD is currently trading at a trailing 30-day interday low—1.3148. The Bank of Canada reinforced resilience in the Canadian economy as it took a neutral stance towards interest rates—becoming one of few countries to maintain interest rates throughout 2019. The decision was supported by inflation rates within the 2% target range—indicative of the Canadian economy operating near capacity. Additionally, signing of the CUSMA reinforced economic ties between Canada, the US and Mexico, providing support for Canadian manufacturers. OPEC also agreed to cut output, resulting in a jump in crude oil prices by nearly 7%. Despite this positivity in key CAD determinants, labour statistics and weaker foreign investment continue to impede further gains for the loonie. The Canadian economy experienced a net reduction of 71.2k jobs in November, increasing the unemployment rate by 0.4%—to 5.9%. The financing of external deficits by deposits indicates that foreign funds continue to enter the Canadian economy; however, the funds are not actively invested—likely due to the ongoing trade war and broader economic uncertainty. Given the current economic conditions, the USDCAD is expected to remain within the 1.32 range through the first quarter of 2020.

Oil Prices

Oil prices are hitting new highs and Saudi Aramco reached its $2 trillion valuation on the second day of trading as OPEC enforces output cuts and investors demonstrate positive sentiments following phase one of the US-China trade war. OPEC also released a statement indicating that the trade slowdown seen in recent months has bottomed out, with expectations of increased industrial activity in 2020. Positivity in the oil markets were reiterated in the prices of the global oil benchmark, Brent, and WTI, which increased in the last month by 8.3% and 16.3%, respectively. Going forward, productivity from India and China—leading global consumers of oil—will determine whether OPEC’s cuts are sufficient enough to raise oil prices.

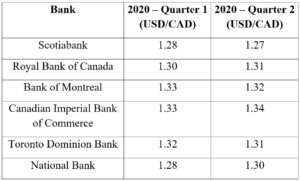

Forecast Table