You check the Mastercard conversion rate before a foreign purchase, see a clean number, and assume that’s what you’ll pay. Then the statement arrives, and the Canadian dollar amount is noticeably higher than you expected.

That gap isn’t a mistake. The Mastercard conversion rate is the starting point of a calculation, not the final price. Foreign transaction fees, dynamic currency conversion at checkout, and the way card networks set their wholesale rates all add cost on top, and most of it never appears as a line item on your statement.

For Canadians making large or recurring foreign purchases (a U.S. property bill, tuition, a winter abroad), those layered costs add up quickly. This guide breaks down how the Mastercard conversion rate actually works, where the hidden costs come from, and how to keep more of your money on every transaction.

What is the Mastercard conversion rate?

The Mastercard conversion rate is the wholesale exchange rate Mastercard uses to convert a foreign currency transaction into your card’s home currency, like Canadian dollars (CAD). It’s the rate that gets applied the moment your transaction is processed, and it’s the rate Mastercard publishes on its currency converter tool.

That rate isn’t the same as the one you see on Google or on the Bank of Canada’s exchange rate page. Understanding the difference is the first step to spotting where your money goes.

The Mastercard scheme rate vs. the mid-market rate

The mid-market rate, sometimes called the interbank rate, is the midpoint between the buy and sell prices for a currency on the global market. It’s the rate banks use when they trade with each other, and it’s the benchmark you see quoted on Google, Reuters, or financial news sites.

Don't Waste Money With Banks.

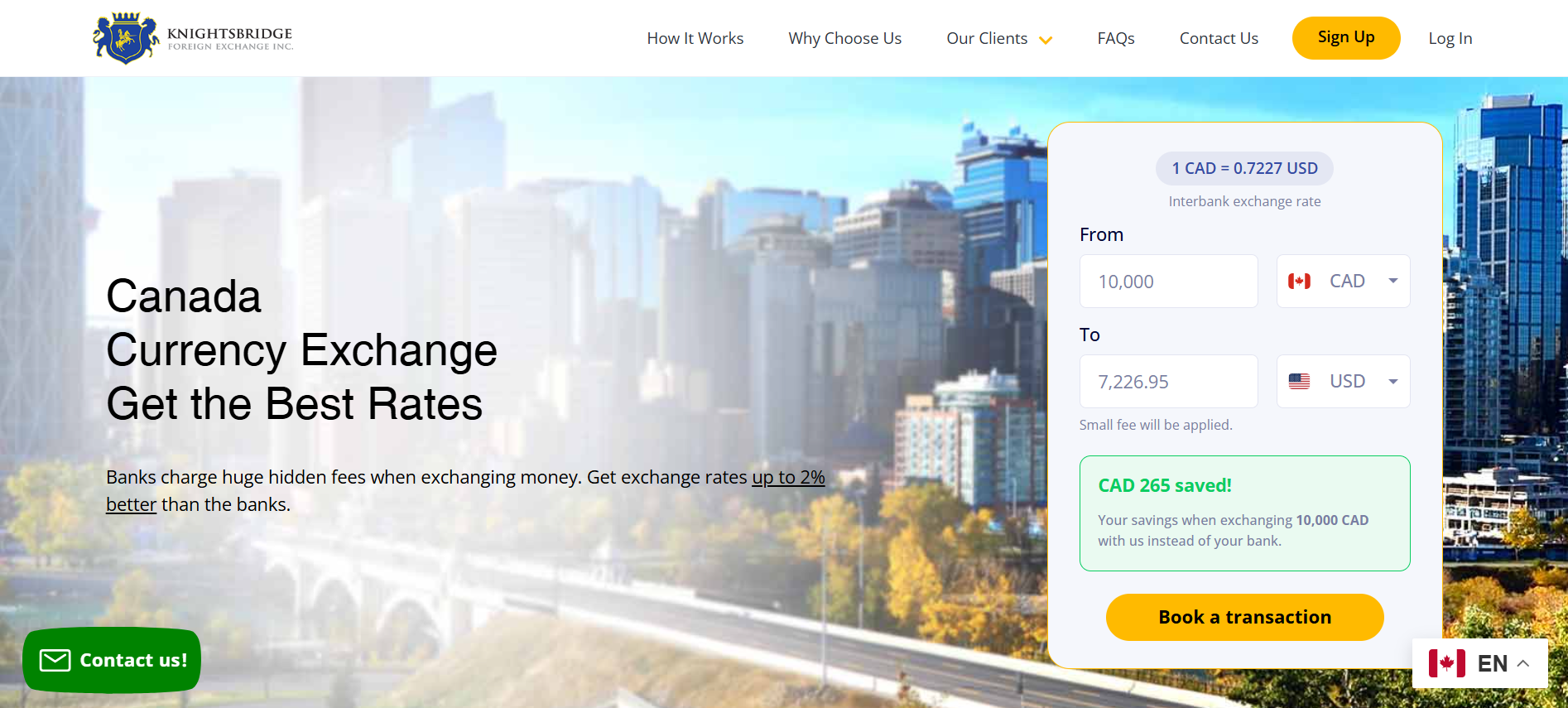

Get Exchange Rates Up to 2% Better With KnightsbridgeFX

The Mastercard scheme rate is a wholesale rate that Mastercard sets each day for converting foreign transactions. It’s calibrated against the global currency market and is generally close to the mid-market rate, but it’s not identical. Mastercard updates its rate once per business day, and the rate that applies to your transaction is the one in effect on the day the transaction is processed, which isn’t always the same day you swiped your card.

For most personal purchases, the gap between the scheme rate and the mid-market rate is small, often a fraction of a percent. The real cost comes from what gets added on top of that scheme rate, which we’ll get to in the next section.

Why the Mastercard conversion rate differs from Google’s rate

When you look up an exchange rate on Google, you’re seeing the mid-market rate at that moment in time. When Mastercard processes your transaction, three things change that number:

- Timing. Mastercard’s rate is set once per business day and applied at the time of processing, not the time of purchase. Currency markets move constantly, so the rate you see on Google at checkout isn’t necessarily the rate Mastercard uses a day or two later.

- The scheme rate margin. Mastercard’s wholesale rate is close to but not identical to the mid-market rate. The small difference is built into how the network operates.

- Layered fees from your card issuer. This is where most of the cost lives, and it’s the part that doesn’t appear on the Mastercard converter at all.

That last point matters most. Most Canadians blame the card network for the markup, but the bigger fees come from your card issuer, not Mastercard itself.

The 3 costs that determine what you actually pay in foreign currency

The Mastercard conversion rate is only one piece of the puzzle. The true cost of a foreign transaction includes layered fees that most cardholders never see broken out on their statements. KnightsbridgeFX believes currency exchange shouldn’t be misleading, so here’s a clear look at every cost stacked on top of the scheme rate.

The Mastercard scheme rate

This is the foundation. The scheme rate converts the foreign currency amount into your card’s billing currency using Mastercard’s wholesale rate for that processing day.

On its own, the scheme rate is competitive. It’s typically within a small fraction of a percent of the mid-market rate, which makes it one of the better wholesale conversion rates available to consumers. If the scheme rate were the only thing you paid, foreign currency purchases on a Mastercard would be reasonably priced.

It isn’t the only thing you pay.

Your card issuer’s foreign transaction fee

This is the fee that quietly inflates almost every foreign Mastercard purchase made by a Canadian. Your card issuer (the bank that gave you your Mastercard, not Mastercard itself) adds a foreign transaction fee on top of the scheme rate, typically 2.5% on Canadian credit cards.

That fee applies any time you pay in a currency other than Canadian dollars, including:

- Online purchases from foreign retailers

- Subscription services billed in U.S. dollars

- Hotel bookings and travel reservations abroad

- ATM withdrawals in foreign currency

On a $5,000 USD purchase, that’s $125 in foreign transaction fees added to whatever the scheme rate converts the purchase to. If you return the item, issuers don’t reverse the foreign transaction fee on refunded transactions, so even cancelled purchases cost you.

A handful of Canadian credit cards waive the foreign transaction fee, but most don’t. If you’re not sure whether yours does, check the cardholder agreement under “foreign currency conversion.”

Dynamic currency conversion (DCC) and how it inflates your bill

Dynamic currency conversion is the option a merchant or ATM gives you to pay in Canadian dollars instead of the local currency. It looks helpful (you see the price in CAD right at checkout), but it’s almost always the more expensive choice.

Here’s what happens when you accept DCC:

- The merchant’s payment processor (not Mastercard) handles the currency conversion at the point of sale.

- They set their own exchange rate, typically with a markup of 2 to 5% above the mid-market rate.

- Your card issuer still charges its 2.5% foreign transaction fee on top of that converted amount, because the transaction still originated in a foreign currency.

The result: you pay the DCC markup and the foreign transaction fee. In some cases, declining DCC and using a no-foreign-transaction-fee card can save you up to 10% on each purchase, both online and in person.

DCC almost always costs you more than letting Mastercard handle the conversion. Always pay in the local currency unless you have a specific reason not to.

Mastercard vs. Visa vs. KnightsbridgeFX: Which gives you the better rate?

For everyday foreign purchases at a coffee shop or hotel, Mastercard and Visa work fine. Both networks use comparable wholesale rates, and the difference between them is usually negligible. The bigger variable is your card issuer’s foreign transaction fee, which is the same 2.5% across most major Canadian banks, regardless of whether the card is Mastercard or Visa.

For larger or recurring foreign currency transfers, like a snowbird funding a winter in Florida, a parent paying U.S. tuition, or a Canadian buying property abroad, card networks fall short. The 2.5% foreign transaction fee alone costs $250 per $10,000 exchanged. On a $100,000 transfer, that’s $2,500 before you account for any DCC markups or ATM fees layered on top.

This is where a specialized currency exchange provider becomes the better tool for the job. KnightsbridgeFX is a Canadian-based foreign exchange company that has served over 150,000 customers since 2009. Its rates consistently beat what card networks effectively charge once issuer fees are included, with no hidden spreads and free wire transfers on every transaction.

A few specifics worth knowing:

- KnightsbridgeFX offers a Best Rate Guarantee on its exchange rates against Canadian banks.

- It holds an A+ rating with the Better Business Bureau.

- It’s registered with FINTRAC, the Canadian government’s financial transactions regulator.

For small everyday purchases under a few hundred dollars, a Mastercard with a no-foreign-transaction-fee card is convenient enough. For anything larger or recurring, a dedicated foreign exchange provider will keep significantly more money in your pocket.

How to optimize your foreign currency transactions

Two practical steps can reduce what you pay on every foreign purchase, starting today.

How to avoid dynamic currency conversion at checkout

When a payment terminal or online checkout asks whether you’d like to pay in Canadian dollars or the local currency, always choose the local currency.

- At a payment terminal abroad. The terminal will display two amounts: one in the local currency and one in CAD. Choose the local currency. If the merchant defaults to CAD without asking, ask them to switch.

- At an ATM abroad. When the ATM asks if you want to “be charged in your home currency,” say no. Decline the conversion and proceed in the local currency.

- At online checkout. Some international retailers default to displaying prices in CAD. Look for a currency selector and switch to the merchant’s local currency before completing the purchase.

The savings are real. Declining DCC on a $1,000 USD purchase can save you $20 to $50 just on the markup, before accounting for any other fees you might avoid.

How to verify the exact conversion rate you were charged

Your credit card statement usually shows the Canadian dollar amount of a foreign purchase, but not the conversion rate or the foreign transaction fee applied. To verify what you actually paid:

- Find the foreign currency amount on your statement (most issuers list both the original amount and the converted amount).

- Divide the CAD amount by the foreign currency amount to get the effective exchange rate.

- Compare that rate to the Mastercard scheme rate for the processing date using the Mastercard currency converter.

- The gap between the two is your foreign transaction fee plus any other markups.

If the gap is much wider than 2.5%, something else is going on, possibly DCC, an unfavorable processing-day rate, or an additional fee from your issuer. It’s worth calling your bank to ask for a breakdown.

For more strategies on reducing card fees on foreign purchases, see how to avoid foreign exchange fees and the 2.5% fee every foreign credit card purchase incurs.

Stop overpaying. Get a better rate than Mastercard on every transfer

The Mastercard conversion rate is a starting point, not the full story. Once your card issuer’s 2.5% foreign transaction fee is added, and once dynamic currency conversion gets layered on top at checkout, the rate you actually pay can be 3 to 5% (or more) above the mid-market rate. On a $50,000 transfer, that’s $1,500 to $2,500 of margin you never see itemized.

For small everyday purchases, a Mastercard with no foreign transaction fees is fine. For larger transfers, recurring payments, or anyone moving meaningful sums across the border, card networks aren’t built to give you the best rate, and the layered fees are designed to be hard to see.

KnightsbridgeFX consistently beats bank and card network rates for Canadian customers, with transparent pricing and human support available by phone, email, and chat. As a Canadian company that has served over 150,000 customers since 2009, KnightsbridgeFX gives you a better rate than the Mastercard scheme on every transfer, with no hidden margins and no surprise fees.

Join thousands of Canadians who bypass bank markups and sign up for a free KnightsbridgeFX account to secure exchange rates consistently better than the Mastercard scheme.

Frequently asked questions about Mastercard conversion rates

Does the Mastercard conversion rate change on weekends?

No. Mastercard updates its conversion rate once per business day, so weekend and holiday purchases get the most recent business day’s rate. The bigger variable is when your transaction is processed. A Saturday purchase might not be processed until Monday, meaning Monday’s rate applies, not Friday’s. For volatile currency pairs, that two-day gap can move the rate noticeably.

Why was my final charge different from the Mastercard rate I looked up?

Three things stack on top of the scheme rate:

- Timing. Mastercard’s rate applies at processing, not at purchase, which can be a day or two later.

- Your issuer’s foreign transaction fee. Usually 2.5% on Canadian cards, added on top of the conversion.

- Dynamic currency conversion. If you accepted “pay in CAD” at checkout, the merchant’s processor handled the conversion at a marked-up rate instead of Mastercard.

Any combination widens the gap between what you looked up and what you paid.

Is Mastercard or Visa better for foreign currency conversion?

For most cardholders, the difference is negligible. Both networks use comparable wholesale rates. What matters far more is your card issuer’s foreign transaction fee (usually 2.5% on Canadian cards), whether you decline dynamic currency conversion, and whether your card waives foreign transaction fees. For larger or recurring transfers, neither network gives you the best rate. A specialized provider like KnightsbridgeFX consistently beats both.

AUD

AUD CAD

CAD EUR

EUR GBP

GBP NZD

NZD USD

USD