Most Canadians assume their bank gives them a fair deal on currency exchange. It doesn’t. Every time you convert Canadian dollars (CAD) to USD, euros, or pounds sterling, your bank quietly builds in a margin. That margin often costs you 2%–3% per transaction, which is hundreds or even thousands of dollars a year if you travel, invest, or send money internationally.

You don’t see this cost as a line item because it’s baked into the exchange rate.

You can do better. When you understand how foreign exchange rates work and how banks price them, you can keep more of your money. The right provider can cut your costs dramatically while giving you more control over exchange transactions.

This guide breaks down how Canadian banks compare, what their services actually cost, and how to keep more of your money.

Which Canadian banks offer the best currency exchange rates?

Before you compare options, you need to understand one thing. Most Canadian financial institutions price currency exchange in similar ways. The difference comes down to how much margin they add, and how transparent they are about it.

Don't Waste Money With Banks.

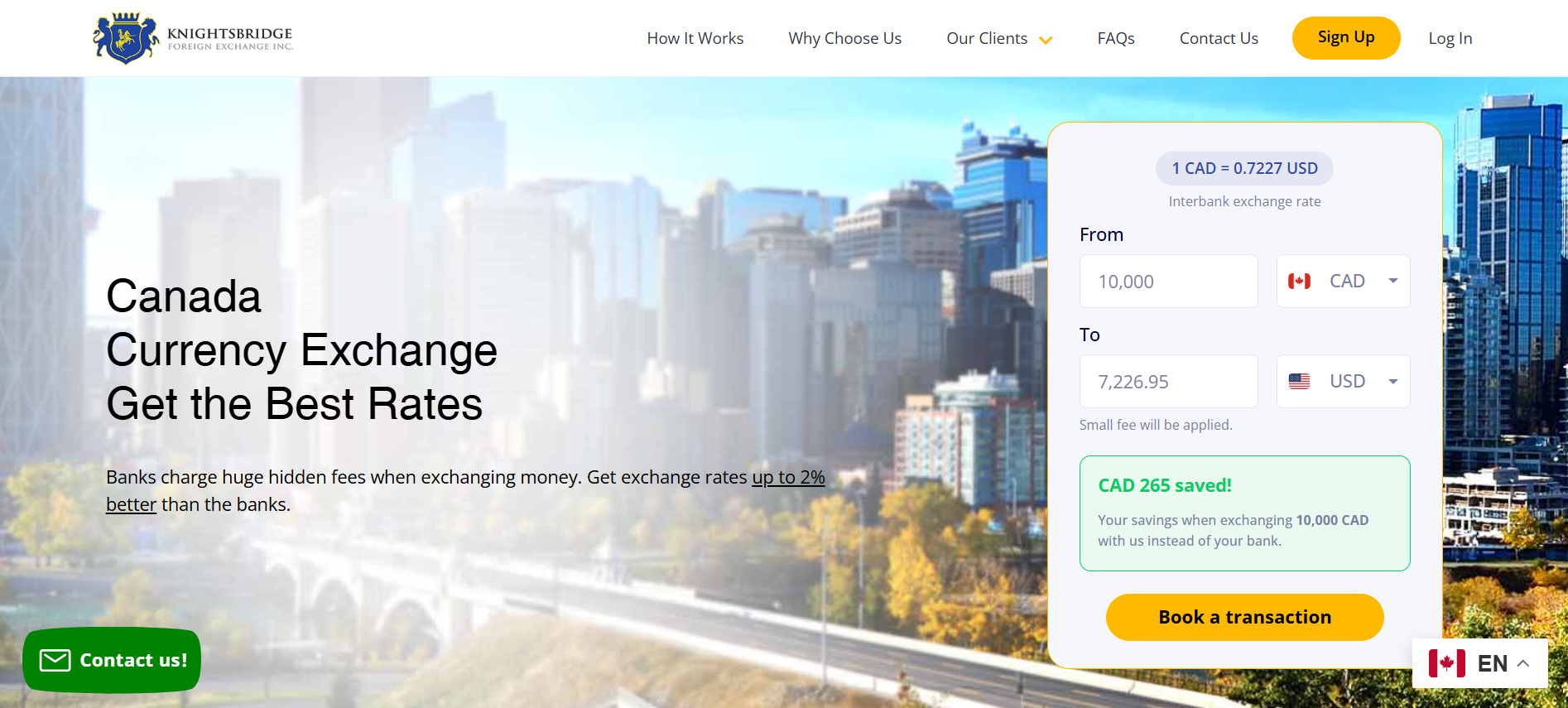

Get Exchange Rates Up to 2% Better With KnightsbridgeFX

Banks focus on convenience. Specialized providers focus on value.

For instance, KnightsbridgeFX takes a different approach because exchanging currency shouldn’t be expensive. Instead of embedding large spreads into rates, it uses volume-based pricing and passes those savings directly to you.

Comparing rates across major banks and credit unions

When you compare exchange rates across Canada’s major banks, you’ll notice small differences, but they all follow the same model.

Here’s what you typically see:

- Large banks (RBC, Scotiabank, TD, BMO, CIBC): These banks offer easy access through your bank account, debit card, or branch. However, their foreign exchange rates often include a spread of 2.0%–3.5% above the mid-market rate. On a $100,000 USD exchange: $2,000 to $3,500 in hidden costs

- Credit unions: Credit unions may offer slightly better conversion rates, especially for members. Still, most rely on the same wholesale providers as banks, so savings are limited.

- Airport and retail exchange kiosks: These providers offer convenience, but rates are often the worst, sometimes exceeding 3%–5% in hidden margins.

You may see small differences between banks on any given day, but these are minor compared to the markup each one applies.

The bigger issue is transparency. Most institutions do not clearly disclose their markup.

- You will not see a line item showing the fee

- You receive a rate that looks reasonable at first glance

- The true cost only becomes clear when compared to a benchmark like the Bank of Canada rate

Verdict: Most Canadian banks and credit unions offer similar rates, and the real cost comes from the markup you rarely see.

Digital platforms and online exchange services

Online currency exchange services have reshaped how Canadians access foreign currency. This is because specialized currency exchange providers offer a clear cost advantage over traditional banks. These platforms focus on:

- Lower overhead than banks

- Transparent pricing

- Faster execution for money transfer and global transfer needs

Common options include fintech apps, currency brokers, and specialized providers.

Here’s how they compare:

- Fintech apps: Offer competitive rates for small transfers and everyday spending, often linked to your debit card or mobile wallet.

- Currency brokers (like KnightsbridgeFX): Designed for larger transactions, such as property purchases, investments, or business payments. You get tighter exchange rate margins and personalized service.

- Bank-owned digital platforms: Still carry bank-level spreads, even if the interface feels modern.

Why many Canadians choose specialized providers:

- Rates closer to the mid-market rate

- Transparent pricing with no hidden spreads

- Online access with no need to visit a branch

If you regularly send money abroad, convert CAD to USD, or deal in currencies like GBP, CHF, or MXN, specialized currency exchange providers consistently outperform banks on cost.

For example, KnightsbridgeFX, a Canadian-owned currency exchange specialist, is built around one principle: currency exchange should not be expensive. Here’s why you can trust it:

- Registered with FINTRAC

- Bank-beating rates with transparent pricing

- No hidden spreads or surprise fees

- Access to real currency specialists for support.

Verdict: For most transactions, specialized currency exchange providers offer better rates, more transparency, and significantly lower overall costs than banks.

How much do Canadian banks charge for currency exchange?

You rarely see a “fee” labeled as a currency exchange charge. Instead, banks make money through the rate itself. To understand your true cost, you need to break down two components: spreads and additional fees.

Understanding exchange rate margins and spreads

Every currency has a real-time mid-market rate, which is the rate you see on a currency converter or from the Bank of Canada. The highest cost isn’t a fee you’ll see on your statement, but the spread built into the exchange rate itself.

The spread is the difference between the mid-market rate (the real rate published by the Bank of Canada or shown on financial news sites) and the rate your bank actually offers. Most Canadian banks apply spreads of 2% to 2.5% or higher on CAD/USD exchanges.

Here’s how it works in practice:

If the mid-market rate for CAD to USD is 1.3500, your bank might offer 1.3838, pocketing the difference on every dollar you convert. On a $10,000 exchange, that 2.5% spread costs you $250. On a $100,000 property purchase or tuition payment, the same spread costs $2,500.

Banks advertise “competitive rates” or “no fees,” but the spread is where they’re actually charging you, and it’s rarely disclosed upfront.

Providers like KnightsbridgeFX work differently, offering rates much closer to the mid-market rate with spreads substantially lower than those applied by banks. That difference is meaningful, especially on larger transactions like CAD to USD conversions for property purchases, tuition, or retirement transfers.

Additional fees for currency exchange services

Beyond the exchange rate spread, Canadian banks layer on several additional charges:

- Wire transfer fees: Most Canadian banks charge $15 to $80 per outgoing international wire, depending on whether you initiate it online, by phone, or in-branch.

- Receiving fees: Some institutions charge $10 to $20 when foreign currency arrives in your account.

- Service and processing fees: Less common currencies often require advance ordering and carry flat processing fees.

- Account maintenance fees: Foreign currency accounts may carry monthly charges, plus conversion costs each time you move funds in or out.

- Delivery charges: Physical foreign currency orders typically add $5 to $15 for courier or branch delivery.

When you stack these fees on top of the exchange rate spread, the total cost of a bank currency exchange can easily reach 3% to 4% of your transaction amount. On a $10,000 USD purchase, that’s $300 to $400 in total costs.

With KnightsbridgeFX, you avoid most of these layers. You get:

- Transparent pricing

- No hidden spreads

- Clear transfer fees (if any) upfront

What currency exchange services do Canadian banks provide?

Banks offer a wide range of foreign exchange services. The trade-off is simple: convenience versus cost. You can access currency exchange almost anywhere, but you’ll pay for that accessibility.

In-branch currency exchange services

Walking into a branch is the most traditional approach, and it comes with the widest spreads in the market, often 2.5% to 4% above the mid-market rate. You’re paying for the overhead of physical locations, teller staffing, and on-hand currency inventory. Many branches also don’t stock significant amounts of less common currencies, so you may need to order ahead and wait several business days.

For small amounts of travel cash, say, $200 to $500 for immediate spending needs, the convenience of an in-branch exchange might be acceptable. For larger transactions like property purchases or tuition payments, the cost difference compared to a specialized provider becomes significant enough to warrant a different approach.

Online and mobile currency exchange options

Most banks now let you exchange currency online through your bank account.

You can:

- Convert CAD to USD or other currencies

- Send money internationally

- Set up recurring transfers

Advantages include convenience from home, integration with your existing accounts, and faster processing times. However, the core issue remains: exchange rates still include wide spreads, and fees for wire and global transfer services still apply.

In contrast, KnightsbridgeFX offers a similar online experience, but with significantly better pricing and dedicated support to guide your transaction.

For occasional small transactions under $500, your bank’s mobile app may be sufficient. But for larger or more frequent exchanges, dedicated currency platforms deliver substantially better value while offering the same digital ease.

Travel money cards and foreign currency accounts

Prepaid travel cards and foreign currency accounts are appealing for frequent travelers, such as snowbirds or those with ongoing foreign currency needs. However, the initial currency conversion still happens at the bank’s marked-up rate, often 2.5% or more above mid-market, plus potential loading fees, monthly maintenance charges, ATM withdrawal fees, and inactivity penalties.

A practical alternative is to convert your funds through a specialized provider first to benefit from better exchange rates, then transfer the foreign currency to your travel card or account for spending. This gives you the convenience of a travel card without paying the bank’s full markup on the conversion.

How to get better exchange rates at Canadian banks

Even within the constraints of traditional bank pricing, a few strategies can reduce the cost of currency conversion.

Timing your currency exchange for better rates

Currency markets move constantly, driven by economic data releases, central bank decisions, and geopolitical developments. CAD/USD tends to be most active during overlapping North American and European trading hours, roughly 8:00 AM to 12:00 PM Eastern Time, when liquidity is highest, and spreads are typically tightest.

Banks also tend to widen their spreads on weekends and holidays, so exchanging on a weekday during business hours generally gives you a better rate.

For larger transactions, monitoring rates over several days and setting a target through your bank’s alert system can help you avoid unfavorable windows. Even perfect timing, though, won’t overcome a poor spread. A bank charging 2.5% above mid-market will still cost you significantly more than a specialized provider offering near-market rates, regardless of when you transact.

Negotiating better rates for large transactions

If you’re exchanging $10,000 or more, it’s worth speaking directly with a branch manager or relationship banker rather than accepting the standard retail rate. Explain the size of your transaction and ask whether they can reduce the spread or waive wire transfer fees. Some banks may offer modest concessions, particularly if you hold a premium account or have a long-standing relationship with the institution.

Even negotiated bank rates rarely approach what dedicated currency exchange providers offer. Before committing to a large exchange, always request a written quote showing the exchange rate, any fees, and the total amount you’ll receive.

For significant sums, comparing your bank’s best offer against a provider like KnightsbridgeFX often reveals thousands of dollars in potential savings.

Stop overpaying for currency exchange

The right currency exchange solution directly impacts how much money you keep.

For smaller, occasional exchanges under $5,000, your bank may be convenient enough. But for larger or more frequent transactions, the cost difference adds up quickly. A $50,000 transfer at a typical bank rate can cost $1,000 to $1,750 more than using a specialized provider.

The better approach is simple. Use your bank for convenience when needed, but switch to a dedicated currency exchange provider for larger transfers where the savings matter most.

Ready to see how much you could save? Sign up with KnightsbridgeFX today to access better rates, transparent pricing, and expert support for all your currency exchange needs.

AUD

AUD CAD

CAD EUR

EUR GBP

GBP NZD

NZD USD

USD