Rebounding housing prices coupled with low lending rates make this a shrewd time for Canadians to consider a property purchase in the United States. Whether you’re in Ontario or Prince Edward Island, purchasing property in the United States can be a great way to increase your net worth, but can be a complicated process. The home buying process in the United States differs in many ways from the Canadian process, and the process by which a Canadian secures a U.S. mortgage is different than that of a U.S. citizen.

Choice of Financing: US Mortgage, Canadian Line of Credit, Home Equity Loan

Once the decision to purchase U.S. real estate has been made, the next decision should be how to finance the property. The most common ways to finance the purchase are through paying the purchase price in its entirety up front, or taking out a mortgage.

It is imperative to outline that Canadians cannot procure mortgages on American properties from Canadian banks. Canadian banks do not have jurisdiction in the United States, and therefore would be unable to seize the property in the event of a default. It is possible to secure a mortgage through one of the banks with cross-border interests, such as RBC or TD, but the arrangement will be with the American arm of the company that is licensed to issue mortgages in the United States.

In assessing how to finance your property purchase, here are some of the more common ways Canadians finance their American property purchases:

Line of Credit (Canadian)

In lieu of taking out a mortgage with an American provider, many Canadians elect to finance their real estate purchase through the use of a personal line of credit. In this process, the prospective buyer would take out a line of credit with his/her banking provider, and purchase the property in the United States in its entirety for cash. The buyer then pays down their line of credit to the Canadian bank, rather than paying a mortgage to an American provider.

Home-Equity Line of Credit

Similar to the use of a line of credit, Canadians can borrow against the accrued equity in their current home to fund the purchase of American property. Loans taken with a home-equity line of credit generally offer better rates than that of a regular line of credit, and buyers can borrow up to 80% of the value of their home through a home-equity line of credit. Unfortunately, this option will be unavailable for those individuals making a first home purchase, or for individuals with insufficient equity in their current home.

Mortgage

Canadians can obtain mortgages from U.S. providers to purchase real estate. However, the process is much more detailed and cumbersome than they are accustomed to in Canada. For example, a mortgage can be secured in a few days in Canada, while the same process will take a Canadian 45-60 days for the purchase of U.S. real estate. The two countries also require different documentation for the procurement of a mortgage, which for which the American document requirements can be found here and here.

Personal Savings/RRSPs

Another option for individuals who have sufficient savings is to pay the purchase price independent of debt financing, through the use of their personal wealth. This is only possible if you have substantial savings at your disposal.

Determining which of these options is best for you will require you to analyze your current financial situation, stage in life, and overall payment preferences, as these will differ between individuals.

Don't Waste Money With Banks.

Get Exchange Rates Up to 2% Better With KnightsbridgeFX

Getting a Mortgage Preapproved

If you elect to finance your home purchase via mortgage, it would be in your best interest to get your mortgage pre-approved by a U.S. mortgage provider before you find the property you intend to purchase. As previously mentioned, the U.S. mortgage approval process is significantly more sluggish for Canadians than the Canadian process. If you wait after you submit your offer for the property to secure your mortgage it might be too late, as it takes 45-60 days for a Canadian to secure a mortgage in the United States.

U.S. lenders will often require down-payments of at least 20-30% for international home purchases, so ensure that if you would like to finance your home purchase with a mortgage that you are looking to make a down-payment of at least this size. Also remember that mortgages will generally cost international purchasers 1-2% more than they would for domestic purchasers, but with the current low lending rates in the United States, it should not be a pervasive problem. You will also be required to produce a number of different documents for your potential creditors to analyze, which can be found here and here.

It is likely that you will need to open a U.S. bank account if you wish to take out a U.S. mortgage. U.S. mortgages are also compounded monthly as opposed to semi-annually in Canada, so this is another notable difference. As a Canadian, it will likely be easier for you to secure a mortgage with a Canadian bank that has reach into the United States, such as RBC or TD. Using a Canadian bank with reach in the U.S. could additionally help you to get a better rate on your mortgage.

Lastly, ensure you consider closing costs and any other unexpected costs you might have to pay in association with your property purchase. Be careful not to overextend yourself with your property purchase, and be sure that you will have sufficient cash flow to cover closing expenses and insurance.

Different types of Mortgages and Mortgage Decisions

If you do decide to pursue the option of taking out a mortgage with a U.S. based company, there are many other decisions you will need to make before you come to an agreement on your mortgage, including:

Open vs. Closed Mortgages

In an open mortgage, you are free to pay down your mortgage payment at any time. You can use bonuses from employment, general savings, or other employment income to pay down the mortgage at a quicker pace than you are otherwise required, offering you financial flexibility.

In a closed mortgage, you are unable or heavily penalized for making advance payments on your mortgage. Instead, you are required to make monthly payments for the entirety of your mortgage. Closed mortgages do often allow for some small lump-sum payments, and often come at a cheaper rate than open mortgages due to their more restrictive parameters. The decision to opt for a closed or open mortgage will depend of how highly you value the flexibility offered by the open mortgage.

Conventional vs. High-Ratio Mortgages

In conventional mortgages, 20% or greater of the home’s purchase price is included as a down-payment. In high-ratio mortgages, less than 20% of the home’s purchase price is included in the down-payment. If you are looking to secure a mortgage as an international buyer, it is likely that you will be required to make a down-payment of at least 20%, making your mortgage conventional.

Mortgage Term

The mortgage term is the length of time for which the contract conditions of the mortgage will be fixed. After the mortgage term expires, the mortgage will have to be renegotiated. Mortgage terms can last for time periods of 6 months, 1 year, 2 years, 5 years, or even longer. In deciding on your mortgage term, look to see what your risk tolerance is. If you would prefer to know what your future obligations will be to the closest extent possible, opt for a longer mortgage term. If you are more risk-inclined, opt for a shorter mortgage term in hopes of negotiating a more favourable deal at the end of the term.

Fixed vs. Variable Interest Rates

In fixed rate mortgages, the interest rate that is paid is locked in for the full term of the mortgage. Payments for the term are set in advance, making it easy for you to plan your payment schedule with a fixed rate mortgage. With a fixed rate mortgage, you need not worry about future interest rate changes over the term period. A fixed rate mortgage will be quoted with an exact interest percentage, such as 5% interest, for the duration of the term.

In variable rate mortgages, the amount of interest paid varies over the term of the loan. The actual payments made will be determined at the onset of the term. What varies is the amount of the payment that contributes to paying down the principal vs. the amount that goes towards paying interest. Variable rate mortgages will be quoted in relation to another rate, usually the prime interest rate, in the fashion of “prime+0.5%”.

The decision between fixed rate and variable rate mortgages depends largely on your risk tolerance. Fixed rate mortgages allow for more predictability, as there is no need to worry about future interest rates for the duration of your mortgage term. However, variable rate mortgages allow you to take advantage of falling interest rates, and can always be converted to a fixed rate mortgage at a later date. This decision is dependent upon risk tolerance and financial flexibility.

Amortization Period

The amortization period is the duration of time in which you will pay your mortgage off. The longer the amortization period, the lower your monthly obligations, but the more interest you end up paying in the long run. It makes financial sense to keep the amortization period as short as possible while still allowing you to live comfortably.

Payment Schedule

The payment schedule details how often you will make mortgage payments. Monthly, biweekly, or even weekly payments are all common payment schedule arrangements. Be sure to select the payment schedule that best fits your bill-paying and budgeting patterns. If you budget monthly, a monthly payment schedule could be convenient. The same applies for weekly and biweekly budgeters.

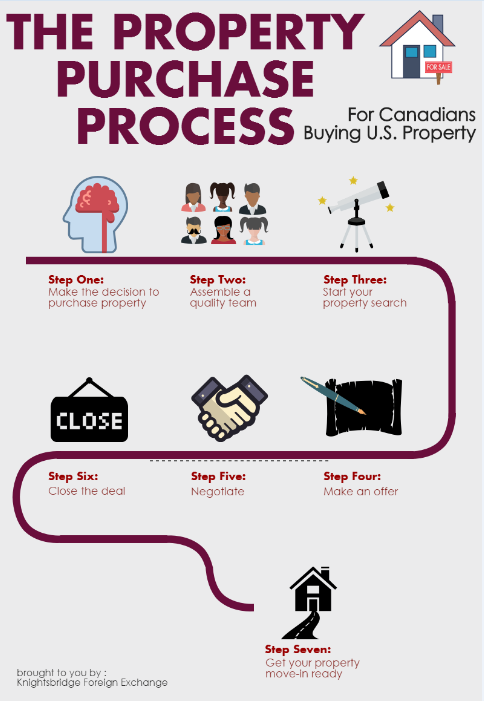

The Property Purchase Process

Step One: The decision to purchase

The first step in the property purchase process is making the decision to purchase a property. Review your finances, your life goals, and what the implications of purchasing the property will be for your lifestyle. Consider the possibility of renting vs. buying. If you decide that purchasing a property is the best idea for your situation, you are ready to begin the process.

Step Two: Assemble a quality team

The key to a smooth property purchasing process is getting the right people in place. The first “team member” you should look to find is a mortgage broker. Securing a mortgage in the United States usually take 45-60 days as a Canadian. It is easiest for you to get a mortgage preapproved before you begin to search for a home, so you know exactly what your budget will be. Having a pre-approved mortgage will also allow you to quickly move to the offer stage in time sensitive situations.

After you’ve gotten a mortgage pre-approved, you should look to add a real estate sales representative to your team. Ensure you secure a representative whom you are comfortable working with, as they will be integral to your property purchase. You should be satisfied with their expertise, as well as comfortable with their fees. Once you find a real estate sales representative, you can begin to assemble the rest of your team, which should include a real estate lawyer (or notary), a home inspector, real estate appraiser, and an insurance broker. Leverage the expertise of your assembled team to the best of your ability, as this will lead to the best results.

Step Three: Start your property search

Inform your realtor of your purchase preferences, and they will begin compiling a list of properties that meet your specifications to show you. You can also curate a list of properties you would like to see by doing some research on the internet, scouring neighbourhoods for “For Sale” signs, or through word-of-mouth. Once you have a list of properties you would like to see, visit them and see which ones you like. This part of the process can take time, as a property purchase is a high involvement purchase.

Step Four: Make an offer

Once you’ve decided what home you want to purchase, you’re ready to begin preparing an Offer to Purchase. Remember that an Offer to Purchase is a binding legal document, so consult both your realtor and your real estate lawyer when drafting it. Consult your property purchase team to help you decide what price you should make in your offer. On more competitive properties, you may be required to make an offer above the listing price. For less competitive listings, or properties that have been on the market for a long time, you might be able to table an offer below the listing price.

You will need to explicitly outline any conditions you have in your offer. Some examples include a satisfactory home inspection report or a property appraisal. Also, ensure you include an exhaustive list of items you want included with the house if that was part of your offer requirements. One of the most common parameters is the inclusion of furniture.

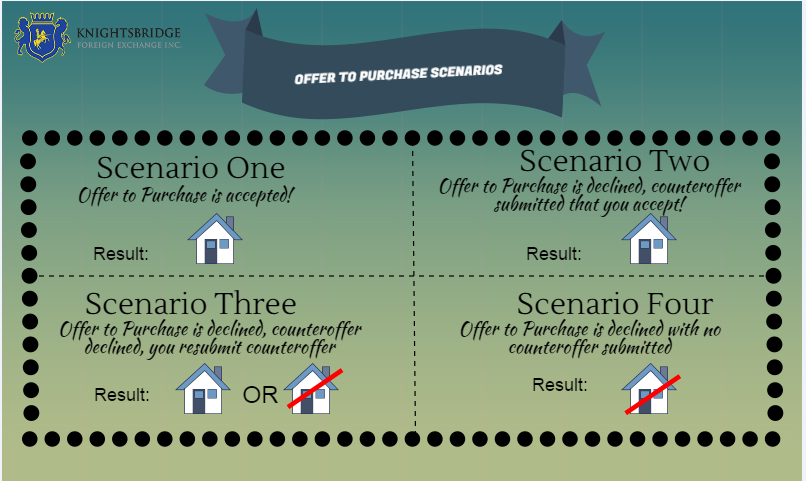

Step Five: Negotiate

When you make an Offer to Purchase there are four distinct scenarios that can arise, conveyed in the following info graphic:

The negotiation can often be unpredictable. Set a maximum limit you are willing to pay for a property, and don’t be afraid to walk away if you find the conditions of a deal unsatisfactory.

Step Six: Closing phase

When you have a mutually agreeable Offer to Purchase, you can begin the closing phase. The closing date will be specified in your Offer to Purchase, usually 30, 60, or 90 days after the offer was accepted. On the closing date, the property officially changes hands, and is now your responsibility. You should have your insurance situation sorted out prior to the exchange, as it will protect you from any unforeseen unfortunate events once the property switches hands. On the closing day, you will pay the down-payment to your lawyer/notary (including any closing costs), and the bank will give your mortgaged funds to the lawyer/notary as well. The lawyer will then transfer the funds to the seller, consummating the contract. The property is now legally yours.

Step Seven: Getting your property move in ready

Once you’ve purchased the property, the final task is to get the property move-in ready. You should change the locks on any new home purchase for security reasons. You will also need to consider moving costs, and decide on your method of moving. Options include hiring professional movers or conducting the move yourself. Be sure to assess whether your home/auto insurance will cover your items during the move should anything happen en route.

Important People in the Property Purchase Process

Real Estate Sales Agent (Realtor)

Your real estate agent will help you buy your property. They will represent you, and be tasked with studying property listings, providing you with market advice, and presenting purchase offers to sellers for consideration. Picking a real estate agent you are comfortable with is of paramount importance, as they can be very influential in the home-buying process.

Mortgage Broker

A mortgage broker is the creditor that grants you a mortgage to finance your home purchase, should you choose to finance your property purchase via mortgage. More details about how to choose what mortgage is right for you can be found above.

Home Inspector

Relying on strong construction knowledge, home inspectors examine previously owned homes for buyers. They look for defects that are not priced into the seller’s price, and they suggest improvements. 35 states require home inspectors to be licensed. If you are purchasing a house, you should have the home inspected first in order to avoid any unforeseen complications with the property.

Real Estate Appraiser

A real estate appraiser studies the local real estate market to help determine a fair value for the house you are looking to purchase, based on a multitude of factors. You should consider the use of a real estate appraiser to ensure you arrive at an accurate property value, so you can make your offer accordingly.

Lawyer or Notary

A real estate lawyer will be required in order to prepare and review transaction documents, negotiate terms and conditions, and assist in the transference of titles. If any legal complications arise during the buying process, a real estate agent will be of use in settling these disputes.

Insurance Broker

Your insurance broker can help ensure you have adequately insured your property as soon as duty of care falls onto you. Ensuring your insurance affairs are in order can help protect you from unforeseen complications, and can protect you during the grey area from the end of the settlement process to the time you move into your property.

Tax Implications of Owning US Property

Owning property in the U.S. comes with some tax implications for international property holders. A few of the major topics will be touched on below:

Estate Taxes

If you pass away with worldwide assets exceeding $5.43 million ($10.86 million for couples), and own U.S. property valued at $60,000 or more, you will be required to file a U.S. estate tax return, even if you are not an American citizen. Your estate will be subject to a 40% tax rate on your U.S. property. If you are a high net-worth individual, this is important to keep in mind.

Capital Gains Taxes

If you sell real estate in the United States, you will be required to pay capital gains taxes. The amount of tax you are required to pay will vary, and you can be subject to more favourable capital gains treatment if you have held the property for over a year. If you hold your U.S. property for less than a year, the proceeds will be taxed at your ordinary income tax rate. If you hold your property for one year or longer, you will receive the more favourable capital gains tax treatment, which will fall between 5%-20%, depending on your income level.

Rental Income Tax

In purchasing U.S. property for the purpose of renting, remember that you will pay tax on the rental income you receive. You will be required to file tax returns in both the United States and Canada, with the U.S. having the first claim on taxing your rental income. You will then file your taxes with Canada, who will tax you on the rental income, but will provide you with a credit for the amount of tax you paid to the United States government.

Helpful Tips

Exchange Rates

When making an international property purchase, your purchase will probably need to be made in the local currency. In the case of Canadians purchasing U.S. property, you will need to purchase your real estate using U.S. dollars.

Home purchases are expensive. Saving even 0.5% on your exchange rate can lead to savings of thousands of dollars on such large amounts, so ensure you shop around to find the best exchange rate. An exchange services provider can also help you convert funds to cover you recurring expenses which will also be denominated in U.S. dollars, such as property taxes and utilities.

Use Cross-Border Planning Specialists

As discussed previously, cross-border transactions have some complicated aspects, especially pertaining to tax. You don’t want to forget to file a U.S. tax report; they will charge you an extra 30% if you do this! The best way to find out about these nuanced details is to consult a cross-border professional, specializing in tax, law, or another discipline that could be helpful to you.

Know Your Credit Score

Make sure you know your credit score prior to trying to secure a mortgage. A poor credit score could cause difficulties in getting a mortgage pre-approved, and could even lead to you paying a higher interest rate. Try to ensure your credit report is in good standing, and while your application for a mortgage is being considered do not make any major purchases on credit until you are approved. It may be tempting to purchase new furniture for your future home while you wait, but resist the temptation.

AUD

AUD CAD

CAD EUR

EUR GBP

GBP NZD

NZD USD

USD