Canadian Dollar Update, October 19, 2021 – Canadian dollar extends gains

USD/CAD Open: 1.2319-23, Overnight Range: 1.2319-1.2381, Previous Close: 1.2379

WTI Oil is at $83.49 and gold is at $1,770.40. US markets are higher today.

For today, USD resistance is at 1.2367. Support is at 1.2343.

- Business Outlook Survey undermines Canadian dollar

- Positive risk sentiment returns as US futures climb.

- New Zealand dollar surges on rate hike outlook and higher commodity prices

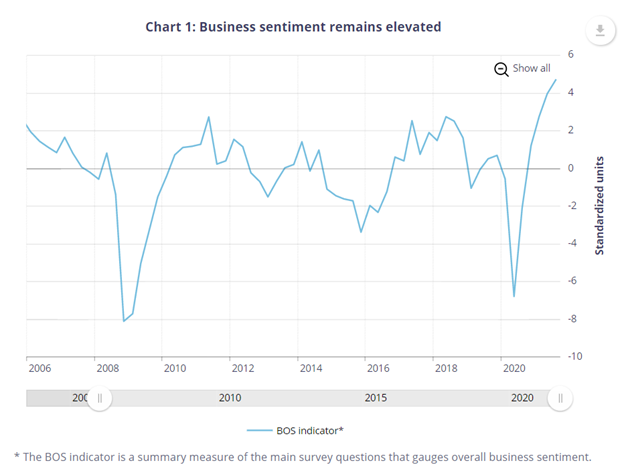

The Canadian dollar surged overnight due to soaring commodity prices and the lingering impact from Monday’s Bank of Canada Business Outlook survey (BOS).

The BOS outlook was very positive as firms anticipate stronger demand as post-pandemic conditions improve. Survey respondents said they “face supply constraints that will limit their sales and put upward pressure on their costs. Together, these demand pressures and supply challenges are driving widespread plans to invest, hire staff and increase prices.”

Business sentiment indicator rose across all areas and most plan to increase capital expenditures.

Source: Bank of Canada

Traders focused on the respondents’ inflation outlook. The survey said, “Almost half of businesses now expect inflation to be above 3 percent over the next two years, with most anticipating it will be between 3 and 4 percent.” Their higher inflation view is due to chain disruptions, fiscal and monetary stimulus and higher food and energy costs.

Some economists suggest the BOS results mean the Bank of Canada will announce that asset purchases will be cut from $2.0 billion/ week to $1.0 billion per week, at the October 27 meeting.

The BOS results served to cap USDCAD gains on Monday and support renewed selling pressures overnight due to rising commodity prices.

The Chinese government ordered power companies to stockpile coal supplies and coal is already near record high prices. Copper prices are also at peak levels. Oil prices recovered from yesterday’s slump and rallied 1.07% overnight due to ongoing fears that demand will outstrip supply into Q1 2022.

The US dollar fell against the major G-10 currencies partly because of increased risks for higher interest rates in many countries while the US interest rate outlook is fully reflected in the greenback.

EURUSD rallied from 1.1610 to 1.1669 due to broad US dollar weakness, and profit-taking. Gains may be limited as ECB policymakers continue to offer dovish outlooks and regard inflation gains as transitory. Finnish Central Bank Governor Olli Rehn said, “The counter evidence speaking for the transitory interpretation is quite convincing. When looking at the longer-term expectations, there is no upward trend…(and) core inflation in the euro area is still subdued.”

GBPUSD climbed to 1.3832 from 1.3727 elevated rate hike expectations after yesterday’s hawkish comments by Bank of England Governor Andrew Baily.

AUDUSD and NZDUSD rallied strongly due to high commodity prices. The RBA minutes did not offer any fresh insight.

The US and Canadian economic calendars are empty.

Today’s Suggested Range USD/CAD: 1.2300 – 1.2400