FX Monthly Outlook – January 2020

Economic Outlook and Summary

The Federal Reserve interest rate currently stands at 1.5-1.75%, with expectations of a neutral stance during their January 28th and 29th meetings. The neutral stance is supported by moderate job growth and inflation, registering an increase in payroll by 145,000, and an inflation rate of 2.3%. Further growth is expected to remain within 2% for 2020, supporting a neutral stance throughout the fiscal year. Further stability was conveyed by the Phase 1 agreement, which, despite any significant progress, will act to stabilize the economy and promote risk-on sentiments for investors. The agreement will allow China to avoid up to $160 billion in tariffs, while maintaining tariffs of up to 25% on approximately $360 billion worth of Chinese goods, and China will maintain tariffs on approximately $100 billion worth of US imports.

The USDCAD has slumped over 5% in 2019, demonstrating significant strength in the loonie. The Bank of Canada is expected to take a neutral stance during Wednesday’s announcement, amidst modest positivity from the jobs report—creating 35,200 jobs in December. Additional support for the loonie was derived from the recently approved USMCA and Ottawa’s fiscal stimulus plan. OPEC’s premature achievement of their January goals and the potential of an Iran-US war also provided temporary support for oil prices and the loonie, prior to de-escalation. Despite the recent positivity surrounding the loonie, the gains are likely short-term, as the stronger loonie will negatively impact the trade-dependent economy. Going forward, the USDCAD is expected to move within the 1.29 range through the first quarter of 2020.

The US Dollar and Federal Reserve

The Federal funds rate remains at the 1.5-1.75% range and is expected to remain unchanged, following recent statistics, during their next meeting on January 28th and 29th. Nonfarm payrolls increased by 145,000, while unemployment held steady at 3.5%—payrolls falling short of the 160,000 jobs consensus. The consumer price inflation rate climbed to 2.3% YoY in December, from 2.1% in November, fueled by an increase in energy costs—rising 3.4% for the month. The broader economy is expected to stabilize in 2020, with growth rates forecasted to record within the 2% range for the year. This growth will be stimulated by risk-on sentiments by investors, as a result of the stability conferred by a Phase 1 Trade Agreement between the US and China.

The US China trade war has subsided following the Phase 1 agreement last week. US officials indicated that China would avoid almost $160 billion in tariffs on their goods, while committing to purchasing billions worth of agricultural goods and oil, and enforcing the regulation of intellectual property theft. Despite the supposed progress, the US will maintain tariffs of up to 25% on approximately $360 billion worth of Chinese imports, while China maintains tariffs on more than $100 billion of US goods. Overall, the Phase 1 agreement hasn’t demonstrated any material progress; however, it has granted stability and positive sentiments for the global economy.

The Canadian Dollar and Bank of Canada

The USDCAD has slumped over 5% in 2019 as it currently trades near its 52-week low, at 1.3066. The most recent increases in the loonie can be attributed to several factors, each acting as independent catalysts of growth in the Canadian economy. Statistics Canada’s recent job report recorded a gain of 35,200 jobs, a reversal from the two previous months of consecutive losses. The report reinforces the Bank of Canada’s stance as the economy remains relatively resilient, despite recent headwinds. Further support was derived from Ottawa’s recently announced fiscal stimulus, as well as the recently approved USMCA. OPEC’s premature achievement of their January goals to cut oil supply would also provide support to the loonie, which benefits from increases in oil prices. Other catalysts, such as the recent escalation between Iran and US, only provided temporary support as oil prices surged in anticipation of expected shortages, should the countries have engaged further. Despite the positivity surrounding the loonie, the significant gains are likely to be short-term, as a stronger loonie will negatively impact Canadian exports, harming the trade-dependent economy. Given the current economic conditions, the USDCAD is expected to move within the 1.29 range through the first quarter of 2020.

Oil Prices

Oil prices experienced a sharp increase in early January as traders became bullish ahead of a proposed Iran-US war—sending crude oil prices above the $65 level. As tensions have subsided, prices have dropped over 9%; however, they still remain relatively high due to recent OPEC cuts and positivity surrounding the US-China Phase 1 agreement. Consistent with previous months, Saudi Arabia over-complied with OPEC’s cuts, compensating for Iraq’s and Nigeria’s over-production. Despite further cuts for 1Q20, OPEC has reinforced the notion of upside potential of growth in demand and increased prices following further cuts of 500,000bpd. Given that their statement relies upon the stabilization of international trade, such as the US-China trade war, any negative developments can significantly alter these projections from OPEC. Furthermore, the proposed cut is likely to only support current prices, rather than raise prices, as the cuts will coincide with a weak quarter for oil demand—relative to other quarters.

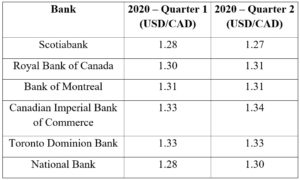

FX Forecast Table