FX Monthly Outlook – November 2019

Economic Outlook and Summary

The Federal Reserve announced an interest rate cut of 25 basis point—to 1.50-1.75%. Quantitative easing continues to provide moderate support for the economy as the reserve continues to repurchase treasury bill—maintaining the funds rate within range. Additionally, the US-China trade war remains unclear as the two parties indicate differing outlooks. Following the implementation of $112 billion in tariffs, China announced that positive concessions are leading to an agreement; however, Trump promptly denied any such progress until demands are met. Despite Trump’s comments, a short-covering rally in oil prices indicated positive sentiments towards a near-term trade deal.

Canada continues to experience current account deficits due to the net outflow of investment, the BoC acknowledges the negative impact of trade-related uncertainty, and Statistics Canada announced a loss of 1,800 jobs for October—contributing to a rise in the USDCAD as it trades above the 1.32 level. Despite this, the BoC chose to maintain a neutral decision as it anticipates growth of 1.5% in 2019, 1.7% in 2020, and 1.8% in 2021. Positive sentiments towards the US-China trade war, resulting in increased consumption and oil prices, may provide support for the loonie. Saudi Arabia’s commitment to elevating Aramco’s IPO will also serve to decrease the USDCAD, as it attempts to boost the price of oil and attain a valuation of $2 trillion. Therefore, the USDCAD forecast remains unchanged at 1.31 by year-end.

The US Dollar and Federal Reserve

The Federal Reserve took a dovish stance during their most recent announcement as interest rates were cut to the 1.5-1.75% range. The decision was aimed at maintaining economic expansion, stronger than expected labour markets, and inflation near 2%—with expectations of continued performance. Quantitative easing will also continue to operate as necessary to maintain the funds rate within target range. The NMI registered 54.7, indicating continued growth in non-manufacturing sectors—2.1 percent higher than September. Non-farm payroll would also increase by 128,000 jobs in October—compared to a consensus forecast of 89,000.

Earlier plans to delay the implementation of tariffs have ended as the U.S. executed $112 billion in tariffs during the first phase of its plan to impose a 15% tariff on $300 billion worth of Chinese goods. China would later announce that positive concessions have resulted in a plan to reduce the tariffs; however, Trump publicly denied the agreement, reinforcing the execution of implemented tariffs. Despite Trump’s US-China trade announcement, positive sentiments were implied by a crude oil short-covering rally as investors displayed renewed optimism for a trade agreement.

The Canadian Dollar and Bank of Canada

The USDCAD currently trades at 1.3227, having increased from October’s low of 1.3053. The USDCAD rally was supported by trade-related uncertainty and its impact on exports and investments, as Canada continues to experience current account deficits—due to net outflow of investments. Still, the BoC opted to maintain neutral interest rates as inflation was within target range at 1.9%—marginally lower than 2%. The decision is currently in line with the mid-term economic performance consensus as the Canadian economy is projected to grow by 1.5% in 2019, 1.7% in 2020, and 1.8% in 2021. However, slightly dismal labour statistics—1,800 jobs lost in October—may prompt near-term expansionary policy as the Canadian economy slows in the second half of 2019. Currently, Canada stands to benefit from the Aramco IPO, if Saudi Arabia takes action to prop oil prices in its attempt to achieve the desired $2 trillion valuation—significant efforts are already evidenced by the latter’s overcompliance with OPEC cuts. Given Canada’s recent positively proportional relationship to crude oil prices, the CAD may find support from the upcoming IPO. Therefore, the USDCAD forecast remains unchanged at 1.31 by year-end.

Oil Prices

Investors will be looking towards OPEC’s official production figures on November 14th to determine the output of its constituents ahead of the early-December meetings. Saudi Arabia has demonstrated their commitment by producing less barrels-per-day than permitted by OPEC and pressuring non-compliant OPEC members. Their approach may be a result of a lower-than-expected valuation of Aramco ahead of its IPO, which can be supported by higher oil prices. Positive investor sentiments were priced in on Friday as short-covering caused a rally in oil prices. The surge in price is indicative of investor optimism of a renewed trade deal, despite Trump’s announcement that a deal was not reached. Currently, oil is holding around the $56 level, significantly higher than October’s lows at $52 level—demonstrating positive short-term price action.

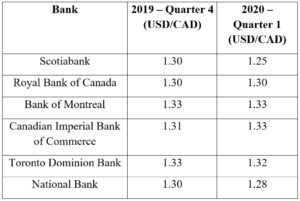

Forecast Table